A Replacement for Keynesian Monetary Policy

How many of these should we make? Image Credit: Freeimages.com/Tracy Olson

As the world confronts the smoking ruin of Keynesian monetary policy [see the posts Economic Damage Created by the Fed, and Why Have ZIRP and QE Failed?, and BOJ Also Losing Credibility and Its QE War, and The Insanity of Negative Interest Rates], some non-Keynesians are discussing what should replace it. Many conservatives prefer the gold standard that preceded our present fiat currency. One example of a nontrivial argument in favor of the gold standard is provided by Nathan Lewis in his post ‘Nominal GDP Targeting’ is Just Another Red Herring To Divide Conservative Monetary Consensus. He notes “conservatives have tended to be split between Stable Money gold-standard advocates, and some form of conservative-flavored ‘soft money.’” Mr. Lewis does not explicitly state what he means by ‘soft money’, but from the context of his discussion it is apparent he means a fiat currency.

Lewis’ post criticizes the idea of a fiat money whose quantity is determined by a procedure targeting nominal GDP (NGDP), as suggested by Scott Sumner, a professor of economics at Bentley University in Waltham, Massachusetts. Dr. Sumner is also Director of the Program on Monetary Policy at the Mercatus Center at George Mason University. Sumner published the ideas Mr. Lewis is criticizing in the Mercatus Center document, A Market-Driven Nominal GDP Targeting Regime. In this paper Sumner states whether or not government overtly manages or monopolizes the actual production of new money is not particularly relevant to the solution of our problems. He writes

In this paper, I will set aside the issues of whether the government should define the medium of account and whether it should maintain a monopoly on producing currency. Instead, I will focus on what I believe is the most important problem in monetary economics: stabilizing the value of the medium of account.

Sumner shows that he definitely has his eyes on what I think is the main prize when he says the most important monetary policy problem is maintaining “the value of the medium of account”, i.e. the value of the dollar. I have written earlier in The Ideal Monetary Policy about how a variable dollar undermines all three of the functions of money. These are: (1) to be the medium of exchange, (2) to be a store of value, and (3) to be the medium of account. All three of these functions are absolutely vital, but the third function is especially critical to the good functioning of an economy. What it means is the economic value of disparate goods and services can be compared by comparing their prices. Goods with higher prices have a higher economic value. In this way one can indeed compare apples and oranges! If money is not allowed to perform this function because of a variable value, then Adam Smith’s Invisible Hand can not perform its magic of balancing supply and demand. Unfortunately, Sumner takes his eyes off of the prize, as we shall see later, when he advocates a procedure for changing the quantity of money that targets a desired nominal GDP.

What is exactly meant by the phrase monetary policy, i.e. what exactly a monetary policy should control, is different with different economists. Sumner identifies the following possibilities for what a monetary policy should be.

- A monetary policy should control the quantity of money.

- Monetary policy should control the price of money, i.e. how much can be bought by foreign currencies, gold, or a basket of commodities.

- Monetary policy should determine the rental cost of money, i.e. short-term and/or long-term interest rates.

The first and second (or indeed the first and the third) of these ways of thinking about the management of money are not necessarily mutually exclusive. Suppose for example, you think the price of a basket of commodities should be kept constant (my own preference), not by price controls, but by changing the quantity of money. That is, you will try to keep the value of money in terms of a basket of commodities constant by varying the amount of money in the system. If the economy grows and the quantity of available goods increases, and if the velocity of money is constant, then the quantity of money must also increase. Otherwise, a constant quantity of money chasing an increased quantity of goods would mean each dollar in terms of the goods it can buy would increase in value; there would be deflation.

As you can well appreciate, thinking about the management of the money supply in any of these ways is fraught with technical difficulties. If you were to approach the problem with my preferences, for example, you would have to choose what commodities go into your basket. The relative values of various goods would be constantly shifting, as we know from the law of marginal utility. By choosing a particular basket of goods, you define a price index whose percent change you would attempt to hold at zero. With a different basket of goods, the changes in the quantity of money required to hold the price index constant would change.

What Sumner proposes to do is to finesse these technical problems. He believes that to target the money supply to yield a stable growth of nominal GDP is more likely to yield better macroeconomic outcomes than to aim for an inflation target. He suggests the Fed could set up a futures market on nominal GDP growth by offering to buy or sell an unlimited amount of futures contracts on nominal GDP. Any institution or individual could participate by buying from or selling to the Fed these NGDP futures. Let us suppose the Federal Reserve wanted to target an annual GDP growth rate of 3%. Then the Federal reserve would buy or sell an unlimited number of contracts where each is valued at one plus the expected growth rate, or $1.03. Any individual who believed the economy would grow at that rate or higher would buy contracts from the Fed for $1.03 each. In the jargon of futures, the participant is going “long” on GDP. In a year’s time the Fed would deliver in dollars the ratio of the new GDP to the previous year’s GDP. If the GDP grew 5%, then it would pay the investor $1.05 and the investor would make a profit of $0.02 on a single contract. If on the other hand the GDP fell 5%, the ratio of the new to the old GDP would be (1-0.05)/1 = 0.95 and the Fed would pay the investor $0.95; the investor would have a loss of $1.03 minus $0.95, or $0.08. If the investor believed the growth rate would be below 3%, he would go “short” by selling contracts to the Federal Reserve for $1.03 each. A short seller would then pay the Fed in a year’s time the ratio of the new GDP to last year’s. If the growth rate was below 3% the short seller would pay the Fed less than $1.03 for each contract and he would profit; if the growth was above that rate, he would have to pay more than $1.03 and he would have a loss.

We will assume market participants are knowledgable and more accurate than not. Then if short sellers were more accurate than those with long positions, i.e. the GDP was less than desired, the Fed would pay more out to the short sellers than it would take in from the long. New money would be injected into the economy. If the long buyers are more accurate than the short sellers, more money is taken out of the economy before the maturity of the contract and the growth rate is moderated. The Federal reserve Open Market Committee (FOMC) would be replaced by this new NGDP futures market.

What Nathan Lewis in his criticism points out is that there are many other factors determining GDP growth rates than just changes in the money supply. For example, if Bernie Sanders were elected President of the United States, his “soak the rich” tax increases and more intrusive regulation of businesses would create a damaged GDP that could not be undone by any changes to the money supply. On the other hand if a new President instituted economy-friendly tax cuts and reductions in regulation, sustainable GDP growth greater than the targeted growth rate could occur. Growth could then be stunted by the NGDP futures market. Much would depend on how well the Federal Reserve could estimate potential GDP growth.

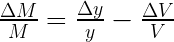

On the other hand, a gold standard that Lewis seems to favor might have its own problems. It is reputed that since economies have on average grown faster than new gold has been produced, a gold standard would seem to be inherently deflationary. However, this is an idea that is more than a little controversial, as Nathan Lewis himself demonstrates. Also, see here and here. As an alternative, let me suggest how a stable currency with a constant buying power can be approximated using fiat money. As I noted in The Federal Reserve and Monetarism, it is fairly easy to show the percent change in the price level is equal to the percent change in the quantity of money plus the percent change in the velocity of money minus the percent change in the GDP. As an algebraic equation, we can write

where P is the price index, M is the quantity of money, V is the velocity of money, and y is the GDP. The Δ operator indicates the change of the quantity on which it operates over a year’s time. Setting the fractional or percent change in price level, i.e. the inflation rate, equal to zero and solving for the change in the quantity of money, we obtain

The previous quarter’s changes in GDP and velocity of money can then tell us how much the quantity of money should be either increased or decreased to keep money’s value constant.

Views: 3,236